As attendance declines across the world, Gaming Intelligence looks at whether other racing jurisdictions will suffer a similar fate to Singapore and Macau’s racecourses

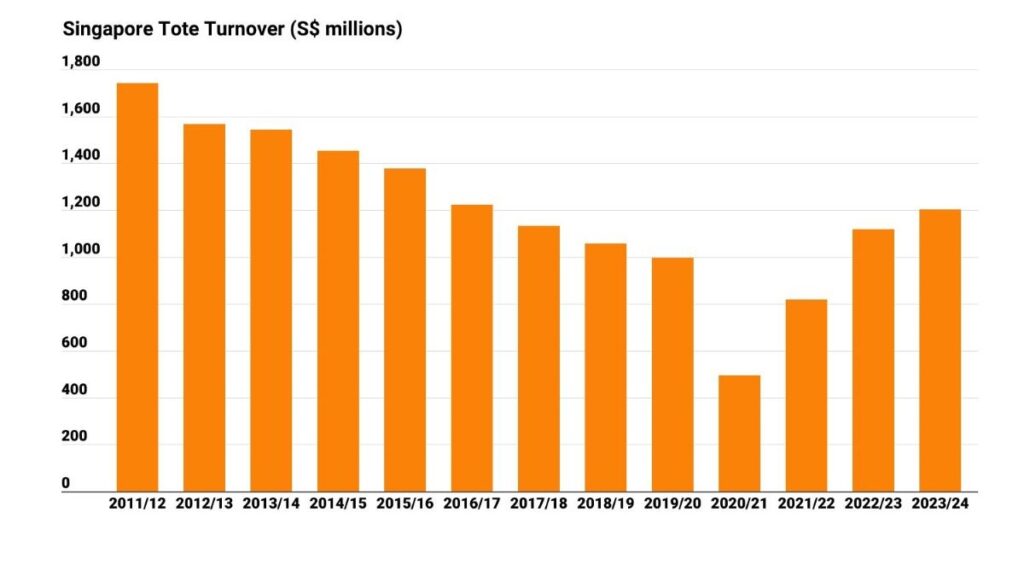

After 182 years, 2024 brought an end to horseracing in Singapore, as 10,000 racegoers gathered at Kranji racecourse in October to witness Smart Star win the last running of the Grand Singapore Gold Cup.

Earlier in the year the Macau Jockey Club ceased thoroughbred horse racing in the SAR after almost 35 years. While Singapore and Macau are the first to close, other racing jurisdictions are wrestling with similar issues that resulted in their demise.

In Macau, a combination of factors had already conspired to cause horseracing’s demise, long before the pandemic made the situation worse. Annual prize money had been falling, which in turn meant the horse population decreased, as did the number of race meetings.

The closure of Kranji racecourse came at a time when Singapore’s wagering on racing was actually increasing and in 2023/24 the Singapore Tote reported its highest turnover in seven years at S$1.20 billion (€836 million).

But attendance at race meetings has been in decline and the reported crowd at the final meeting was only about a third of Kranji’s 30,000 capacity.

Singapore’s racecourse will be used for new housing, as the country has a rising population of more than 6 million people and a limited land area to develop. Racecourses – and golf courses – are a luxury use of land which Singapore can no longer indulge.

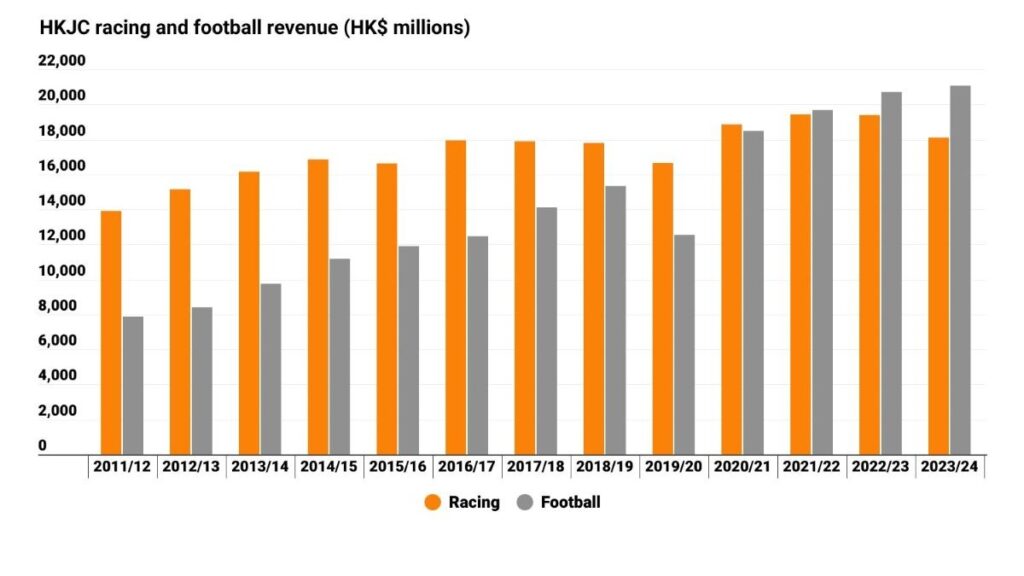

Hong Kong is another racing jurisdiction where land is at a premium, but it is unlikely that either Sha Tin or Happy Valley racecourses will be closed for housing, even though average meeting attendance has been falling.

Average attendance at Happy Valley, for example, was 13,200 in 2024, 31 per cent lower than the 2019 average.

Wagering on horseracing in Hong Kong was HK$105.0 billion (€12.5 billion) in 2023/24, excluding co-mingling pools, with limited year-on-year growth in recent years. The Hong Kong Jockey Club now takes more bets on football than horseracing and also earns more annual revenue from football.

The Hong Kong Jockey Club does still pay more duty on racing than football, even with the new special football betting duty. In 2023/24, racing duty was a substantial HK$13.13 billion (€1.56 billion).

Japan remains the largest racing jurisdiction by wagering and has been growing for more than a decade since 2011, when the country was hit by a devastating earthquake and tsunami. In 2015 total racing turnover hit JPY3 trillion for the first time in seven years and surpassed JPY4 trillion in 2021 (€24.1 billion).

Racing’s wagering growth in Japan has not been matched by racecourse attendance, which has been in decline. Attendance stood above 12.5 million in 2006 but fell below 10 million in 2011.

In 2023, Japan’s racecourse attendance was still 25 per cent lower than the pre-pandemic total at 7.1 million.

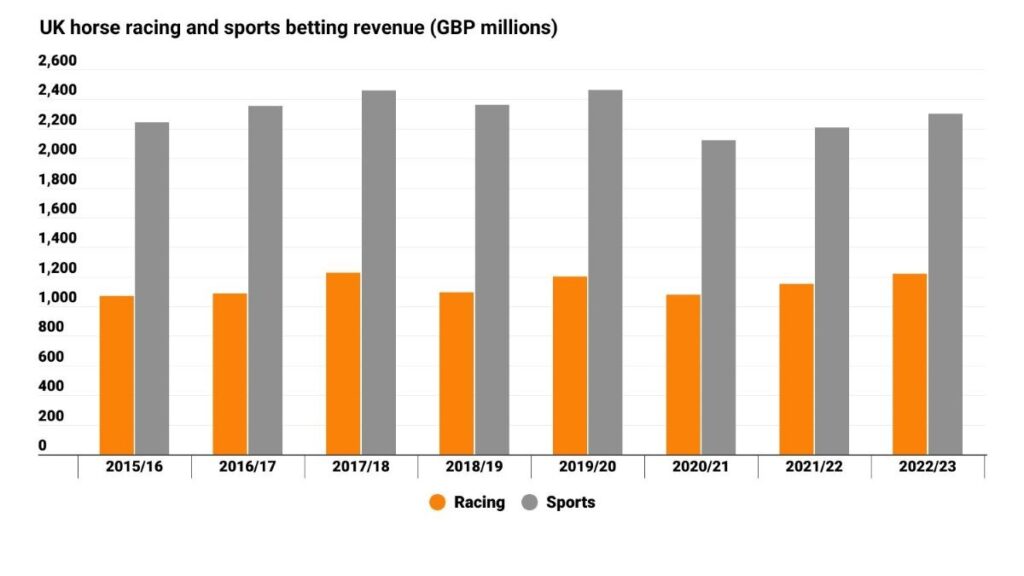

In Europe, UK racecourse attendance has also been under pressure for several years. Annual attendance in 2019 was 5.62 million, which was the lowest total since 2012, at that point. After the disruption of the pandemic, attendance fell below 5 million in both 2022 and 2023, being 4.83 million for each year.

Attendance in the first nine months of 2024 was down by 3 per cent on the previous year to 3.92 million, but a reduction in the number of race meetings meant that average attendance was up by 1 per cent to 3,642.

The British Horseracing Authority (BHA) reports that betting turnover on British horseracing fell by 9 per cent in the first nine months of 2024 compared with the same period of 2023, and by 18 per cent on 2022.

UK Gambling Commission data shows that gross win from horserace betting, including international races, increased by 6 per cent to £1.22 billion in the financial year 2022/23, and was the highest for five years. But horseracing now only accounts for about a third of all UK gross win from betting.

Horse racing in the United States has faced more competition from regulated sports betting, since the repeal of PASPA in 2018. But US racing wagers have held up well and were above $12 billion in both 2021 and 2022. Wagers fell by 4 per cent in 2023 to $11.66 billion, but this was still higher than the $11.26 billion reported in 2018.

For 2024, US racing wagers are estimated to be $11.4 billion, based on data for the first nine months of the year.

There have, however, been several racecourse closures in the US in recent years, including the likes of Arlington Park, Illinois, and Golden Gate Fields, California. In September 2024, it was announced that Freehold Raceway in New Jersey, the oldest racetrack in the US, will close. There had been racing at Freehold Raceway since the 1850s.

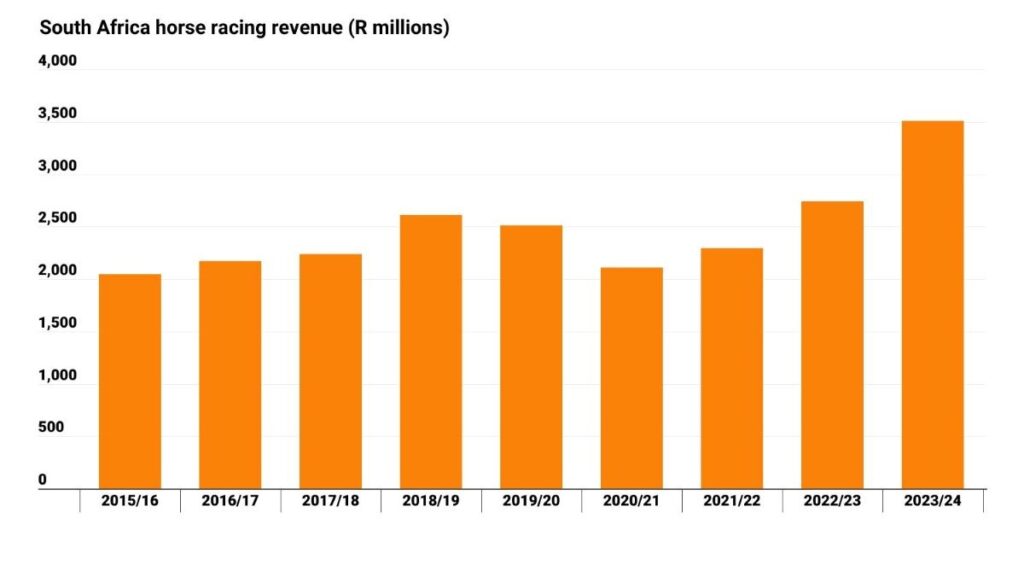

South African horseracing has suffered racecourse closures too and there are just seven racecourses remaining in the country.

Despite the declining number of racecourses, revenue from horserace wagering is at record levels and hit R3.51 billion (€183.1 million) in 2023/24.

All the growth in horserace betting is being driven by South Africa’s bookmakers, as Tote revenue is in decline. The split of revenue in the latest financial year was 89 per cent from bookmakers and just 11 per cent from the Tote.

South Africa’s sports betting sector is growing strongly because of online casino ‘betting’ and, although horserace wagering is gaining some benefit by association, its share of all betting revenue is falling. The share of revenue from horserace wagering dropped below 10 per cent in 2023/24, having been at 65 per cent a decade previously.

Across several key horseracing markets, the trend has been for wagering to be resilient but for racecourse attendance to be in decline.

Attendances were falling in the years before the pandemic but its impact in 2020 and 2021 should not be underestimated in exacerbating the situation.

The pandemic’s disruption caused people to change their behaviour and find other interests and ways to spend their leisure time. Inflationary pressures in the years since the pandemic have also raised the cost of a day at the races in certain markets.

If racecourse operators cannot keep their tracks financially viable, jurisdictions like Singapore and South Africa show the risk of them being sold for housing and other commercial development.

This can lead to a spiral of decreasing numbers of race meetings, lower attendances, a shrinking horse population and fewer betting opportunities on domestic racing.